- Tom

- blockchain, Crypto, News

- 0 Comments

- 13686 Views

UAE to adopt global crypto tax reporting framework

1/ Key takeaways

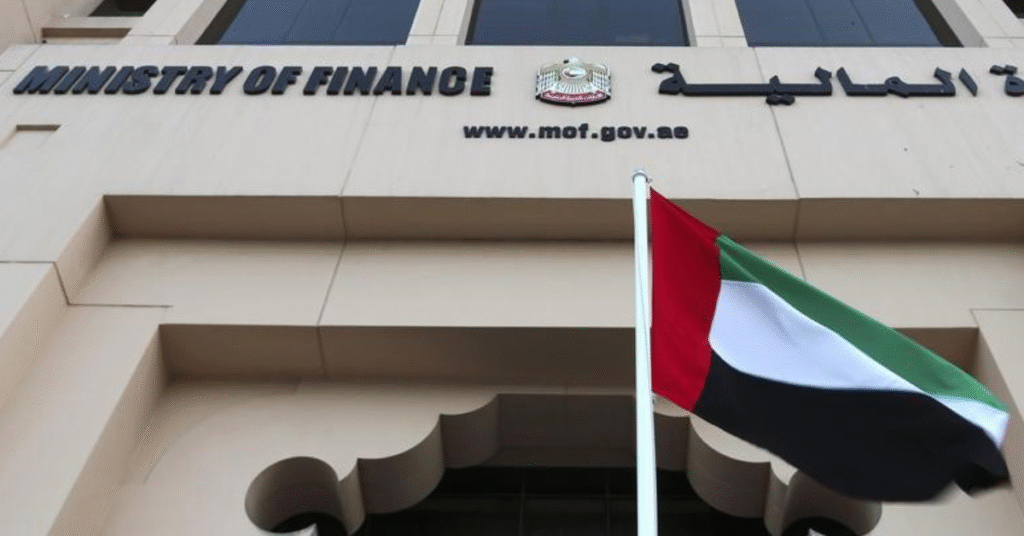

The UAE Ministry of Finance has signed the Crypto-Asset Reporting Framework (CARF), an agreement developed by the OECD to automatically exchange tax information on crypto transactions. This adoption, with implementation starting in 2027, aims to align the UAE with global tax transparency standards while also providing clarity to the crypto industry.

2/ UAE to adopt global crypto tax reporting framework

The United Arab Emirates Ministry of Finance has signed the Multilateral Competent Authority Agreement on the Automatic Exchange of Information under the Crypto-Asset Reporting Framework (CARF), marking a step toward aligning with global tax transparency standards.

Implementation is scheduled to begin in 2027, with the first exchanges of information expected in 2028. The framework, developed by the Organisation for Economic Co-operation and Development (OECD), establishes a system for automatic sharing of tax-related data on crypto-asset transactions across jurisdictions.

In a statement, the ministry said the adoption of CARF would provide clarity and certainty to participants in the crypto sector, including custodians, trading platforms, intermediaries, and advisory firms, while ensuring the UAE upholds international tax compliance obligations.

The move follows the government’s November 2024 announcement of its intent to adopt the framework, part of broader financial reforms positioning the UAE as a regulated yet competitive hub for digital assets.

To shape its national implementation, the ministry has opened a public consultation running from September 15 to November 8, 2025. Stakeholders across the crypto industry are invited to provide feedback on the framework’s potential impacts and areas requiring clarification.

Officials indicated the consultation aims to produce rules that are both aligned with global standards and responsive to market realities.

3/ Hola Tech’s pov:

Based on the recent developments, here are the key next steps and advice for stakeholders in the crypto industry.

3.1/ Actively participate in the public consultation

The most immediate and critical step is for stakeholders to engage with the public consultation, which is open until November 8, 2025. This is the primary opportunity to influence how the Crypto-Asset Reporting Framework (CARF) is implemented. It’s a chance to provide feedback on potential impacts, raise concerns about specific requirements, and suggest clarifications to ensure the final rules are both globally aligned and responsive to local market realities.

– For Businesses (exchanges, custodians, brokers): Provide detailed feedback on the operational and technical challenges of implementing the new reporting requirements. Highlight areas that could create unnecessary burdens or confusion, such as data collection, due diligence procedures, and transaction categorization for decentralized finance (DeFi) or complex financial instruments.

– For Individuals (traders, investors): Comment on the potential clarity or lack thereof for various taxable events, such as airdrops, staking rewards, and transfers between wallets. Seek guidance on record-keeping best practices and how to prepare for future reporting obligations.

– For Advisory Firms: Offer expertise on how the framework can be structured to provide maximum clarity and certainty for all market participants, drawing on international precedents and best practices.

3.2/ Prepare your systems and operations

With the official implementation date set for 2027, crypto businesses must begin preparing their internal systems and compliance protocols now.

– Data Collection & Management: Review and upgrade systems to collect and store the necessary user and transaction data. This includes obtaining self-certifications of tax residency from all users. Systems need to be able to meticulously track and categorize transactions by type (e.g., crypto-to-fiat, crypto-to-crypto) and aggregate data for annual reporting.

– Due Diligence: Enhance your Know Your Customer (KYC) and anti-money laundering (AML) protocols to include the new tax residency verification requirements. This is a foundational step for compliance.

– Reporting Infrastructure: Develop or acquire the necessary technology to generate reports that comply with the CARF’s specific XML schema for automatic information exchange.

3.3/ Seek professional guidance

The adoption of CARF introduces complex tax and regulatory requirements. It is crucial for both businesses and individuals to consult with licensed tax and legal advisors.

– For Businesses: Work with experts to understand your specific reporting obligations as a “Reporting Crypto-Asset Service Provider” (RCASP). Develop a comprehensive, cross-border compliance strategy if you operate in multiple jurisdictions.

– For Individuals: Consult with a tax professional, especially if you are an expat in the UAE with tax residency in another country. Your home country’s tax authority will now have visibility into your crypto activities in the UAE. An advisor can help you understand your tax liabilities and develop smart tax-planning strategies, such as record-keeping and potentially offsetting gains with losses, if such provisions are adopted.

3.4/ Stay informed and adapt

CARF is part of a broader, global shift towards greater transparency in the digital asset space. Stakeholders should continuously monitor for updates and guidance from the UAE Ministry of Finance and the OECD. This includes staying abreast of how other jurisdictions are implementing CARF, which could provide valuable insights and a competitive edge.

Want to stay ahead of the curve in the world of decentralized technology and AI? Check out Hola Tech blog for more exciting technology news and useful information!

author

I leverage my skills in strategic planning, team coordination, and technology solutions as the Co-founder and COO of Hola Tech. Passionate about innovation and efficient problem-solving, I am dedicated to pushing the boundaries of what is possible in the tech industry with Hola Tech

{kind=link}